All Categories

Featured

Table of Contents

The method has its own advantages, but it likewise has issues with high charges, complexity, and more, causing it being concerned as a fraud by some. Infinite banking is not the finest policy if you need only the investment element. The boundless banking idea revolves around the use of entire life insurance policy plans as a monetary tool.

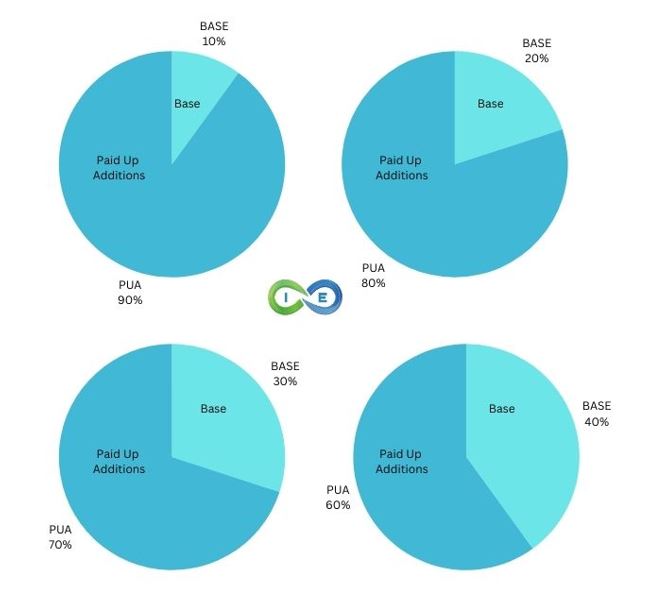

A PUAR permits you to "overfund" your insurance plan right as much as line of it coming to be a Changed Endowment Contract (MEC). When you utilize a PUAR, you swiftly enhance your money worth (and your fatality advantage), thus enhancing the power of your "bank". Additionally, the more cash money worth you have, the better your rate of interest and reward repayments from your insurer will be.

With the surge of TikTok as an information-sharing platform, financial recommendations and methods have actually discovered a novel means of spreading. One such method that has been making the rounds is the boundless banking concept, or IBC for brief, amassing endorsements from stars like rap artist Waka Flocka Flame - Wealth building with Infinite Banking. While the approach is currently preferred, its origins trace back to the 1980s when financial expert Nelson Nash presented it to the world.

How does Infinite Wealth Strategy create financial independence?

Within these plans, the cash worth grows based upon a rate set by the insurance firm. As soon as a substantial cash money value builds up, policyholders can obtain a cash money worth lending. These lendings differ from traditional ones, with life insurance policy functioning as security, suggesting one could lose their insurance coverage if loaning exceedingly without sufficient money value to support the insurance coverage expenses.

And while the appeal of these policies appears, there are natural limitations and threats, requiring diligent cash value tracking. The technique's legitimacy isn't black and white. For high-net-worth people or business proprietors, particularly those utilizing methods like company-owned life insurance (COLI), the benefits of tax obligation breaks and substance growth can be appealing.

The allure of limitless financial doesn't negate its obstacles: Expense: The fundamental requirement, a permanent life insurance coverage policy, is costlier than its term equivalents. Eligibility: Not everybody gets entire life insurance policy due to strenuous underwriting processes that can leave out those with details health and wellness or way of life conditions. Complexity and threat: The complex nature of IBC, combined with its risks, may deter lots of, especially when easier and much less risky choices are available.

Can Private Banking Strategies protect me in an economic downturn?

Assigning around 10% of your month-to-month revenue to the plan is simply not viable for most people. Component of what you read below is just a reiteration of what has currently been stated over.

Before you get yourself right into a situation you're not prepared for, understand the adhering to first: Although the idea is frequently marketed as such, you're not really taking a car loan from on your own. If that were the instance, you would not have to repay it. Instead, you're borrowing from the insurance provider and have to settle it with passion.

Some social media articles suggest making use of cash value from whole life insurance coverage to pay down credit scores card debt. When you pay back the funding, a part of that rate of interest goes to the insurance company.

What is Life Insurance Loans?

For the first several years, you'll be paying off the commission. This makes it very difficult for your policy to build up value during this time around. Whole life insurance policy costs 5 to 15 times much more than term insurance. A lot of people just can not afford it. So, unless you can manage to pay a couple of to several hundred bucks for the next decade or more, IBC won't function for you.

If you require life insurance policy, here are some important tips to take into consideration: Take into consideration term life insurance. Make sure to shop about for the finest rate.

What are the risks of using Cash Value Leveraging?

Imagine never having to fret concerning bank car loans or high rate of interest rates again. That's the power of infinite banking life insurance.

There's no set loan term, and you have the liberty to pick the repayment routine, which can be as leisurely as paying off the loan at the time of fatality. This flexibility includes the servicing of the fundings, where you can choose for interest-only settlements, keeping the finance equilibrium flat and convenient.

What financial goals can I achieve with Infinite Banking For Retirement?

Holding money in an IUL taken care of account being credited interest can typically be far better than holding the cash on down payment at a bank.: You've always desired for opening your own bakery. You can borrow from your IUL policy to cover the initial costs of renting out a room, acquiring equipment, and hiring team.

Individual fundings can be obtained from typical financial institutions and credit report unions. Obtaining money on a credit report card is generally extremely expensive with yearly portion rates of passion (APR) commonly reaching 20% to 30% or even more a year.

{kind=link}

Table of Contents

Latest Posts

Generation Bank: Front Page

Infinite Banking Definition

Ibc Concept

More

Latest Posts

Generation Bank: Front Page

Infinite Banking Definition

Ibc Concept